🎯 Efficient Frontier — Guide¶

“Find the mix that thrills you without keeping you up at night.”

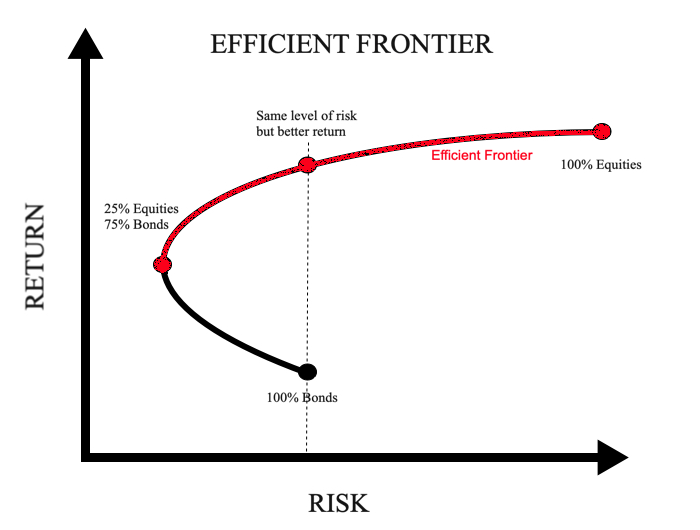

📌 1 What on earth is an efficient frontier?¶

Picture every possible portfolio of your chosen assets on a two‑axis chart:

- X‑axis: annualised volatility (risk)

- Y‑axis: expected annual return

Most dots live in the middle. The efficient frontier is the upper‑left edge of that cloud — the set of portfolios that deliver the highest return for a given level of risk (or, flipped around, the lowest risk for a chosen return).

If your portfolio sits below that curve, you’re either leaving money on the table or accepting more stress than necessary.

💡 2 The intuition before the equations¶

- Diversify: mix assets that don’t move in perfect lock‑step.

- Risk–reward trade‑off: extra risk can buy extra return, but not automatically.

- Optimise: let math churn through millions of weight combinations and keep only the “best so far”.

That’s the whole trick. No black magic required.

📐 3 A pinch of maths (kept gentle)¶

For a portfolio with weights w, the expected return \( \mu_p \) and volatility \( \sigma_p \) are

where

- \( \boldsymbol{\mu} \) — vector of mean asset returns

- \( \Sigma \) — covariance matrix of those returns

To trace the frontier we repeatedly solve:

(Here we forbid short‑selling. Remove \( \mathbf{w} \ge 0 \) if you’re fine with shorts.)

🧪 4 Doing it in code (five lines, promise)¶

ef_returns, ef_vols = construct_efficient_frontier(

returns=my_returns, # DataFrame of daily % returns

tickers=my_tickers,

num_points=100

)

PortfolioPlotter.plot_efficient_frontier(

port_vols, port_returns, sharpe,

ef_vols, ef_returns, max_idx

)

construct_efficient_frontier loops over 100 target returns, feeds each optimisation to cvxpy, and stores the resulting risks.

plot_efficient_frontier colours random portfolios by Sharpe ratio so you can spot the sweet spot instantly.

🖼️ 5 How to read the picture¶

- Black line: efficient frontier

- Red dot: portfolio with the highest Sharpe ratio among the random samples

- Sea of dots: random portfolios — most are, frankly, mediocre

Slide leftwards until lowering volatility starts to shave more return than you’re willing to lose. That’s usually your “happy place”.

✅ 6 Quick checklist¶

- [ ] Use at least three years of daily data (more is better).

- [ ] Annualise returns and volatilities (* 252) consistently.

- [ ] Inspect the covariance matrix for weird outliers.

- [ ] Decide on constraints (no shorts? max weight per asset?).

- [ ] Run the backtest after fixing weights; don’t peek at the future.

📚 Further reading¶

- H. Markowitz — Portfolio Selection (1952)

- Grinold & Kahn — Active Portfolio Management

- Quantocracy blog posts on efficient‑frontier visualisations

(This guide is for educational purposes only — not investment advice.)